The future of commerce isn’t coming—it’s already here, operating in the shadows of blockchain networks. While humans debate the potential of artificial intelligence, autonomous AI agents are quietly conducting business on their own, processing $73 million across 176 million transactions in just twelve months. This isn’t speculative fiction anymore; it’s a measurable economic reality that’s reshaping how we think about money, automation, and market structures.

The numbers tell a story that most people haven’t grasped yet. Software is buying services from other software, and it’s happening at a scale that would have seemed impossible just a few years ago.

The Micro-Transaction Economy: Why 31 Cents Changes Everything

The most revealing statistic isn’t the $73 million total—it’s the 31-cent average transaction size. This figure exposes the fundamental difference between human commerce and machine commerce. These AI agents aren’t making large purchases; they’re conducting constant, tiny transactions for API access, cloud resources, data feeds, and AI inference.

This micro-transaction pattern mirrors historical shifts in commerce. Just as the invention of the telegraph enabled rapid, small-scale financial communications in the 1800s, blockchain rails are enabling a new form of commerce that traditional payment systems simply can’t handle efficiently.

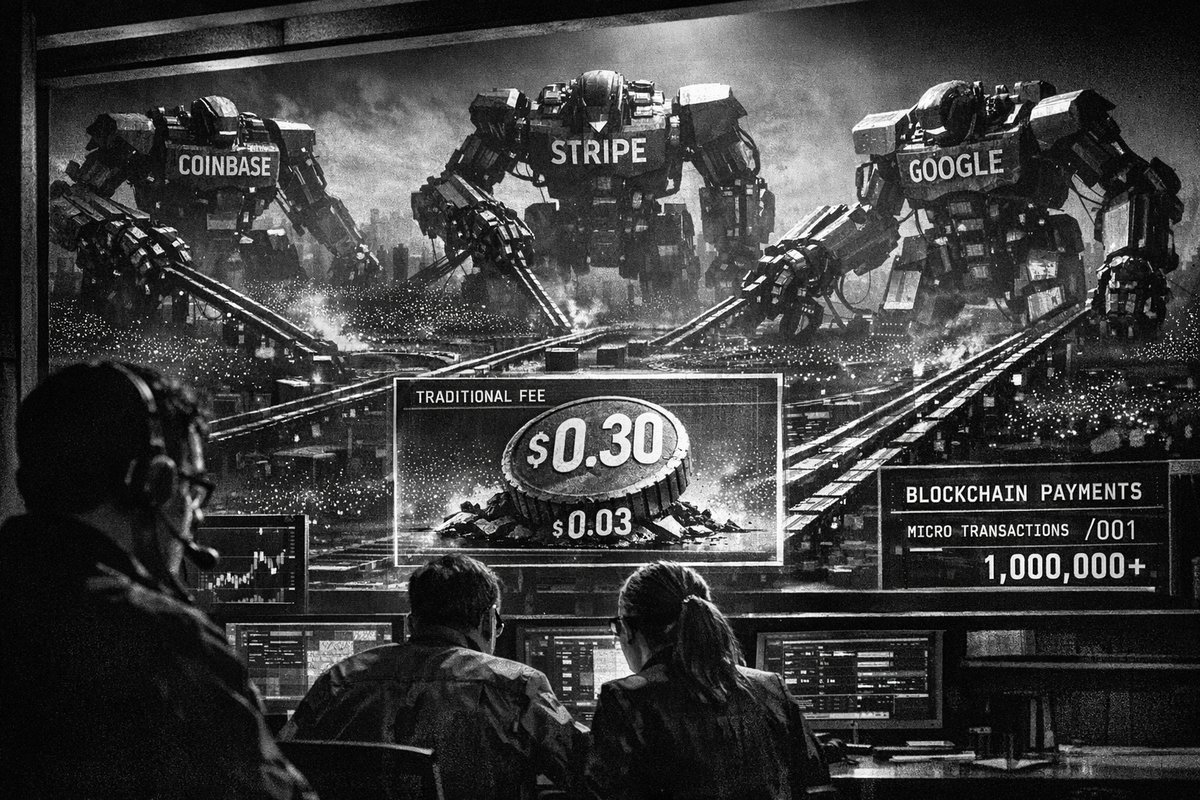

Consider the economics: Visa’s fixed-fee structure costs around 30 cents per transaction. For a human buying a $50 item, that’s negligible. For an AI agent paying 3 cents for a weather API query, the transaction fee costs ten times more than the actual purchase. It’s economically absurd—like paying $10 in postage to mail a penny.

Why Blockchain Became the Default Infrastructure

This economic mismatch explains why 98.6% of autonomous AI agent payments occur using USDC on blockchain networks. It’s not about crypto evangelism or technological trendiness—it’s about basic math. Networks like Base and Tempo enable settlement at fractional pennies, making sub-dollar transactions financially viable at massive scale.

The concentration around USDC creates something historically significant: a standardized settlement layer for machine commerce. This level of asset concentration (98.6%) is reminiscent of the early days of international trade, when gold became the dominant medium of exchange not through government mandate, but through practical necessity and network effects.

“the agent + crypto narrative makes sense to me but maybe people are looking at the boring version of it. software agents can use existing rails for a while. you can spin one up, give it access to tools, connect payments through a human-owned account, and duct tape a lot of the rest together. it’s not perfect, but good enough for a long time.” — @rish_neynar

This perspective captures the current reality, but underestimates how quickly the “duct tape” solutions are being replaced by purpose-built infrastructure.

The Corporate Land Grab: Big Tech Enters the Game

Once the economic case became undeniable, the corporate response was swift and decisive. Coinbase launched x402 for direct USDC payments by AI agents. Stripe partnered with Tempo on its Machine Payments Protocol. Google developed AP2 for delegated spending authorization. Even Visa is expanding infrastructure with tokenized credentials for AI-powered transactions.

These aren’t small pilot programs—they represent a $8 billion commitment in acquisitions and infrastructure investments. The message is clear: established financial companies see machine commerce as a potentially dominant new payments layer, not a niche experiment.

The strategic implications are staggering. We’re witnessing the early stages of a new financial infrastructure stack, and the companies that control the rails will have enormous influence over the machine economy.

The Scale That’s Coming: From Millions to Trillions

Current machine payments represent a tiny fraction of global commerce—Visa alone processes $14.5 trillion annually. But the trajectory is unmistakable. Gartner forecasts AI agents facilitating $15 trillion in purchases by 2028. McKinsey estimates retail agentic commerce reaching $3-5 trillion by 2030.

These projections echo historical technology adoption curves. The internet represented less than 1% of global communications in 1995, yet by 2005 it had fundamentally restructured entire industries. The pattern is familiar: early adopters build infrastructure during the “too small to matter” phase, then benefit enormously when mainstream adoption arrives.

Key indicators of this emerging economy include:

- 104,000+ autonomous AI agents registered across 15+ directories by Q1 2026

- 176 million blockchain transactions in 12 months

- 98.6% market concentration in USDC settlements

- $8 billion in corporate infrastructure investments

- Sub-penny transaction costs enabling micro-commerce viability

The Regulatory Void: Moving Faster Than Law

Here’s where things get genuinely concerning. The technology is operational, the economics are proven, and corporate infrastructure is being built—but the regulatory framework is essentially nonexistent. Europe’s MiCA, the US GENIUS Act, and the EU AI Act are all expected around mid-2026, yet none specifically addresses autonomous machine-to-machine commerce, agent authentication systems, or liability frameworks.

This regulatory gap creates profound questions: Who’s responsible when an AI agent makes an unauthorized purchase? How do you verify machine identity? What happens when software disputes a transaction?

Historically, financial regulations have lagged behind technological innovation, often by decades. The banking regulations we use today were largely shaped by crises in the 1930s. We’re potentially building a multi-trillion-dollar machine economy with 1930s-era legal frameworks.

“AI agents are already users, and they interact with interfaces completely differently than humans do. They don’t scroll, they don’t guess, they parse… A design system built only for humans will maybe break when the user is a machine.” — @ceciliavlso

This insight highlights how deep the transformation runs—we’re not just changing payment systems, but rebuilding the entire interface between commerce and technology.

The Quiet Revolution That Changes Everything

Autonomous AI agent payments represent more than a new payment method—they’re evidence of a fundamental shift in economic agency. For the first time in history, software can independently purchase resources, make decisions about value exchange, and operate in markets without human intervention for each transaction.

This is comparable to the invention of the corporation in the 1600s, which created legal entities that could own property and conduct business independently of their human creators. AI agents are becoming economic entities that can transact independently of their human operators.

The revolution is happening quietly, one 31-cent transaction at a time. While humans debate AI safety and regulation, machines are already building their own economy—and the early infrastructure choices being made now will determine who controls the commanding heights of tomorrow’s automated marketplace.

The question isn’t whether machines will dominate commerce—it’s whether we’ll build the guardrails before they do.

Published in Stream · Dispatch #382 · May 25, 2026 · 5 min read.

Reply to paolo@mont3.ch - every email gets a human answer within 24h.