66% of Americans are already using AI for financial advice, but most are doing it wrong. The problem isn’t the technology—it’s the prompts. MIT’s Andrew Lo cuts straight to the chase: “there’s a real art and science to prompt engineering,” especially when your money is on the line.

This isn’t about being tech-savvy. It’s about understanding how to extract valuable financial guidance from systems that can either illuminate your path or lead you off a cliff. The difference lies entirely in how you ask the question.

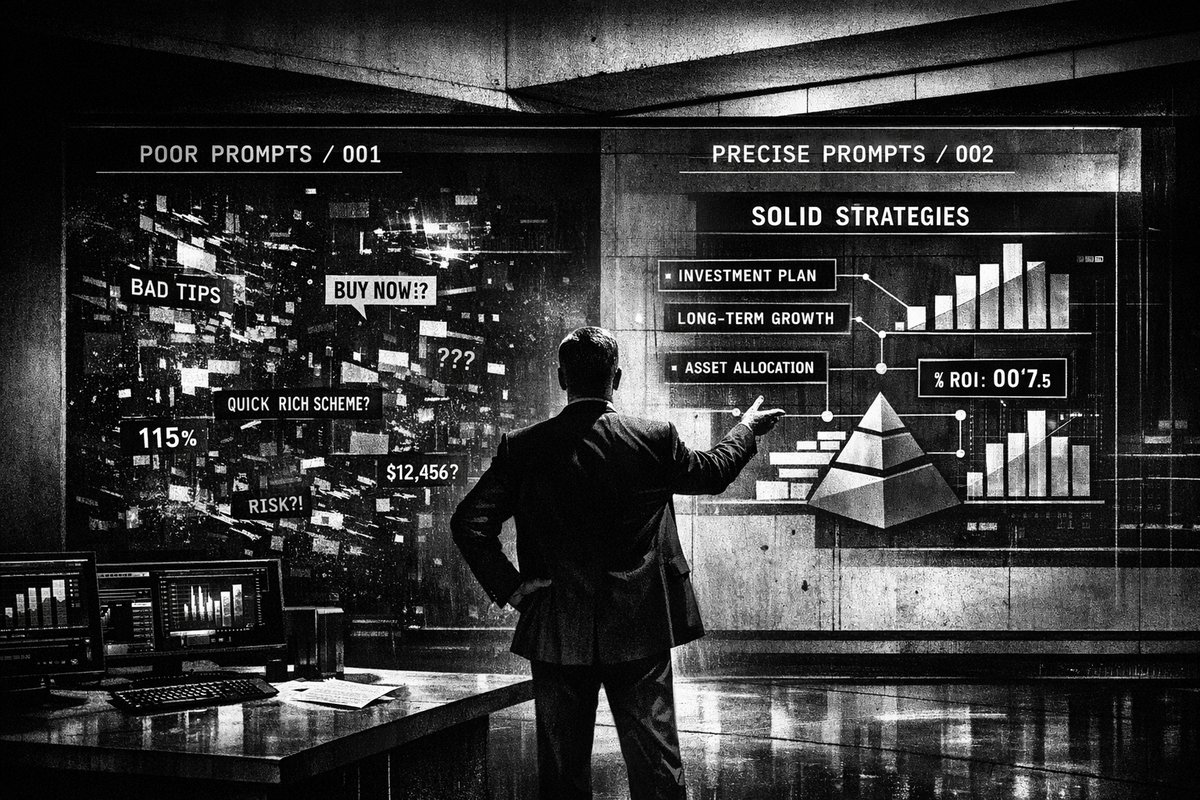

Why AI Financial Advice Fails (And When It Works)

AI excels at high-level financial education—explaining why diversification matters or comparing ETFs to mutual funds. But it stumbles badly on specifics. Tax calculations are a prime example where AI’s confident-sounding answers can cost you real money.

“One of the things about large language models that I find particularly concerning is that no matter what you ask it, it’ll always come back with an answer that sounds authoritative, even if it’s not,” Lo warns. This authoritative confidence is AI’s most dangerous feature for financial planning.

The core issue? AI hallucination—when algorithms generate plausible-sounding but incorrect information. Unlike a human financial advisor who might say “I don’t know,” AI will confidently provide wrong calculations for your tax situation or retirement projections.

The Prompt Engineering Revolution: From Garbage to Gold

Here’s where the art of prompt engineering becomes critical. Consider these two approaches:

Bad Prompt: “How should I retire?” Good Prompt: “Assume you are a fee-only fiduciary advisor. Here are my goals, constraints, tax bracket, state, assets, risk tolerance and timeline. Provide me with: 1) base case strategy, 2) key assumptions, 3) risks, 4) what could invalidate this plan, 5) what information you’re missing.”

The difference is stark. The first generates generic advice. The second creates a structured framework that forces AI to think like a professional advisor bound by fiduciary duty.

This mirrors the evolution of search engines. Early Google users who learned advanced search operators got dramatically better results than those typing random keywords. Today’s AI prompt engineering follows the same pattern—specificity and structure win.

“Google Gemini is the smartest AI right now. But 90% of people prompt it like ChatGPT. That’s why I made the Gemini Mastery Guide: → How Gemini thinks differently → Prompts built for Gemini → 2000+ AI Prompts” — @NextGenAi5

The Reverse Engineering Strategy

Lo introduces a game-changing technique: reverse engineering successful prompts. After getting a satisfactory answer through multiple iterations (often 20+ prompts), ask this crucial question: “What prompt should I have asked you in order to generate the answer that I was looking for?”

This approach creates reusable prompt templates for similar financial scenarios. It’s essentially teaching AI to teach you how to communicate with it more effectively.

Critical Follow-Up Questions That Expose AI Limitations

Never accept AI financial advice at face value. Always follow up with these uncertainty-revealing questions:

- What information did you not have to make this recommendation?

- How convinced are you this is correct?

- What uncertainties exist in your answer?

- What could lead to unreliable outcomes?

- What sources are you drawing from?

Certified Financial Planner Brenton Harrison emphasizes requiring AI to list sources and limit them to credible criteria. Without this verification step, you’re getting opinions, not researched advice.

The Historical Context: We’ve Been Here Before

This AI prompt engineering evolution resembles the 1990s internet research revolution. Early web users who learned to evaluate sources, cross-reference information, and understand search mechanics got vastly superior results. Those who blindly trusted the first result they found often got burned.

The democratization of financial advice through AI mirrors how online brokerages disrupted traditional wealth management in the 2000s. E*TRADE and Charles Schwab suddenly gave retail investors access to tools previously reserved for professionals. But access without education led to the day trading disasters of the dot-com era.

The Generational Divide in AI Adoption

The data reveals a stark pattern: over 80% of millennials and Gen Z use AI for financial advice, compared to lower adoption rates among older generations. This echoes the mobile banking adoption curve—younger users embrace new financial technologies faster, but also face higher risks from inexperience.

85% of users act on AI financial recommendations, according to Intuit Credit Karma research. This high action rate makes prompt quality absolutely critical.

The Bottom Line: Use AI, But Use It Right

AI financial advice isn’t going away—it’s accelerating. The question isn’t whether to use it, but how to use it effectively. The key principles:

- Structure your prompts with specific context and desired output format

- Always question the AI’s certainty and ask about missing information

- Verify sources and cross-check important calculations

- Treat AI as a research tool, not a replacement for professional advice

- Iterate through multiple prompts rather than accepting first answers

The future belongs to those who master AI prompt engineering as a core financial literacy skill. Like learning to read financial statements or understanding compound interest, knowing how to extract reliable guidance from AI systems will become essential for managing money in the digital age.

The art of AI prompting isn’t just about better answers—it’s about avoiding costly mistakes that confident-sounding algorithms can lead you into.

Published in Stream · Dispatch #216 · April 18, 2026 · 4 min read.

Reply to paolo@mont3.ch - every email gets a human answer within 24h.