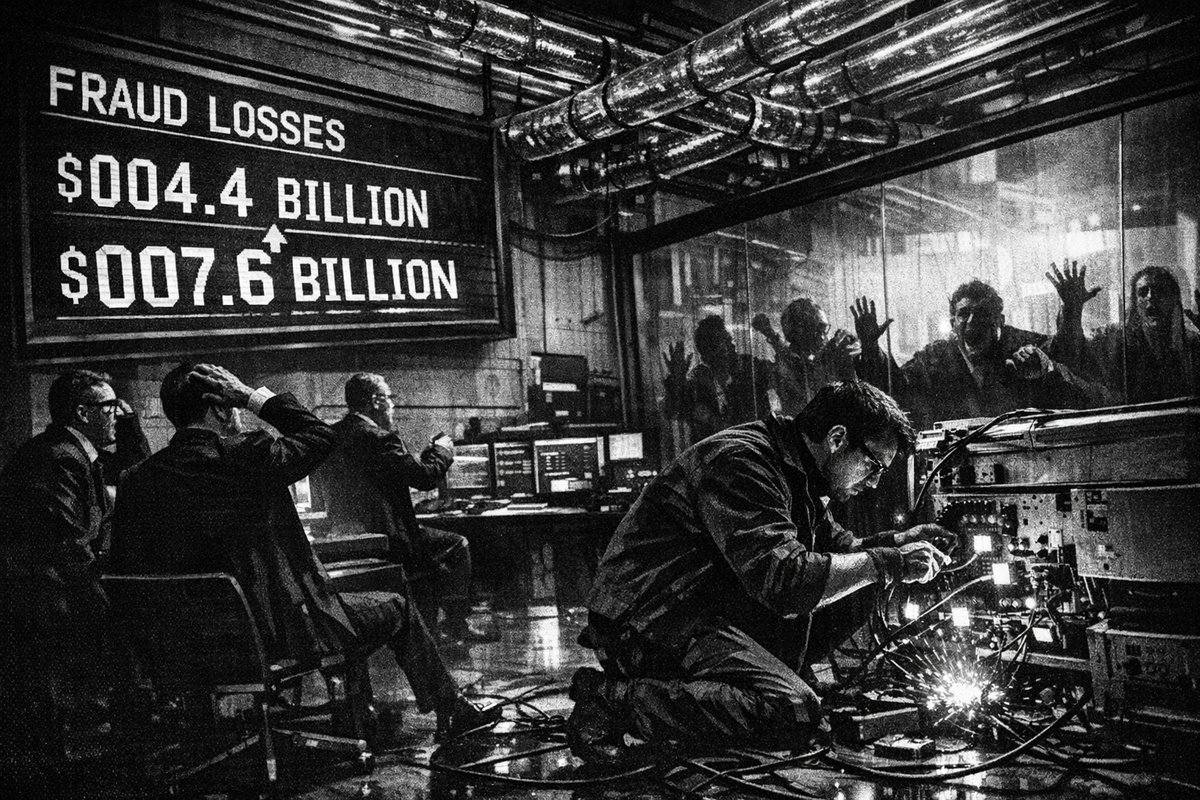

The numbers are staggering and they should terrify every bank executive on the planet. Authorized push-payment (APP) scams are bleeding the global financial system dry at an unprecedented rate—$4.4 billion in losses right now, racing toward $7.6 billion by 2028. Yet most banks are still fighting tomorrow’s fraud wars with yesterday’s weapons.

While fraudsters have evolved into sophisticated, real-time operators, traditional banking infrastructure remains stuck in a reactive mindset that’s about as effective as bringing a telegraph to a smartphone fight. The partnership between J.P. Morgan’s Kinexys and ACI Worldwide represents a rare moment of institutional clarity: the recognition that instant payments demand instant verification.

The Real-Time Rails Revolution Is Backfiring

Here’s the brutal reality banks don’t want to admit: 63% of APP fraud losses currently happen on real-time payment rails, and that figure is projected to hit 80% within three years. This isn’t just growth—it’s an explosion.

The parallels to historical technological disruptions are impossible to ignore. When the telegraph revolutionized communication in the 1840s, it also created entirely new categories of fraud that existing systems couldn’t handle. Similarly, when credit cards emerged in the 1950s, banks initially relied on manual verification processes that proved laughably inadequate for electronic transactions.

The difference today is speed and scale. Modern fraudsters operate in milliseconds while banks validate in minutes—or worse, hours after the damage is done.

“JPM’s vision: instant, invisible, real-time frictionless payments JPMorgan runs on $ZBCN” — @CKJCryptonews

The social media reaction reveals the disconnect between institutional marketing and operational reality. Banks promote “frictionless” experiences while customers lose billions to fraud.

Blockchain: Finally Living Up to the Hype

Kinexys Liink operates as what the company calls one of the “world’s first” bank-led peer-to-peer blockchain networks for data sharing. The technical architecture is payment rail-agnostic, meaning it works across ACH, wire transfers, and instant payment systems simultaneously.

This isn’t the speculative blockchain hype of 2017. This is institutional-grade infrastructure solving real problems:

- Account validation across 70+ countries before money moves

- Real-time verification embedded directly into payment workflows

- Data privacy controls that keep sensitive information secure

- Unified fraud architecture replacing fragmented, channel-specific tools

The historical precedent here is striking. During World War II, the development of RADAR technology transformed from experimental concept to battle-tested system in just a few years because the stakes demanded it. Banks now face a similar moment: evolve or hemorrhage billions.

The Post-Transaction Monitoring Fallacy

Marc Trepanier from ACI Worldwide cuts to the core issue: “When payments settle in real time, verification must have happened prior to the transaction in real time as well.” This seems obvious, yet most banks still rely on post-transaction monitoring—a strategy about as effective as locking the vault after the robbery.

The technical integration embeds account and payee verification directly into payment workflows through ACI Connective, a cloud-native platform that unifies account-to-account payments, card payments, and AI-driven fraud prevention.

Consider this: when SWIFT launched in 1973, it revolutionized international banking by standardizing communication protocols. The Kinexys-ACI partnership represents a similar standardization moment for real-time fraud prevention.

The Compliance Pressure Cooker

Banks aren’t just fighting fraud—they’re battling regulatory expectations and reimbursement pressures that make traditional reactive approaches financially unsustainable. Gloria Wan from Kinexys acknowledges this reality: institutions must “adapt to a rapidly changing landscape” where customer protection isn’t optional.

The public reaction on social media tells the story banks don’t want to hear:

“please report - 9072282385 9422853193 9262931597 7508314493 they specifically call sbi folks… there’s an uncle i know, and i asked him for some help. it turns out the data was leaked somewhere, and even he doesn’t know they are calling people using his name” — @planetgauri

This isn’t abstract fraud statistics—it’s real people losing money while banks scramble to implement basic verification systems that should have existed years ago.

The $7.6 Billion Wake-Up Call

The projected escalation to $7.6 billion in global APP fraud losses by 2028 isn’t inevitable—it’s what happens when institutions fail to match technological capabilities with operational realities. The Kinexys-ACI partnership demonstrates that blockchain technology has finally matured beyond cryptocurrency speculation into mission-critical financial infrastructure.

Banks that continue treating real-time fraud as a post-transaction problem will find themselves explaining billion-dollar losses to regulators, customers, and shareholders who have run out of patience for excuses. The technology exists. The integration strategies are proven. The only question remaining is which institutions will act before the next fraud wave hits.

Published in Stream · Dispatch #259 · April 27, 2026 · 4 min read.

Reply to paolo@mont3.ch - every email gets a human answer within 24h.