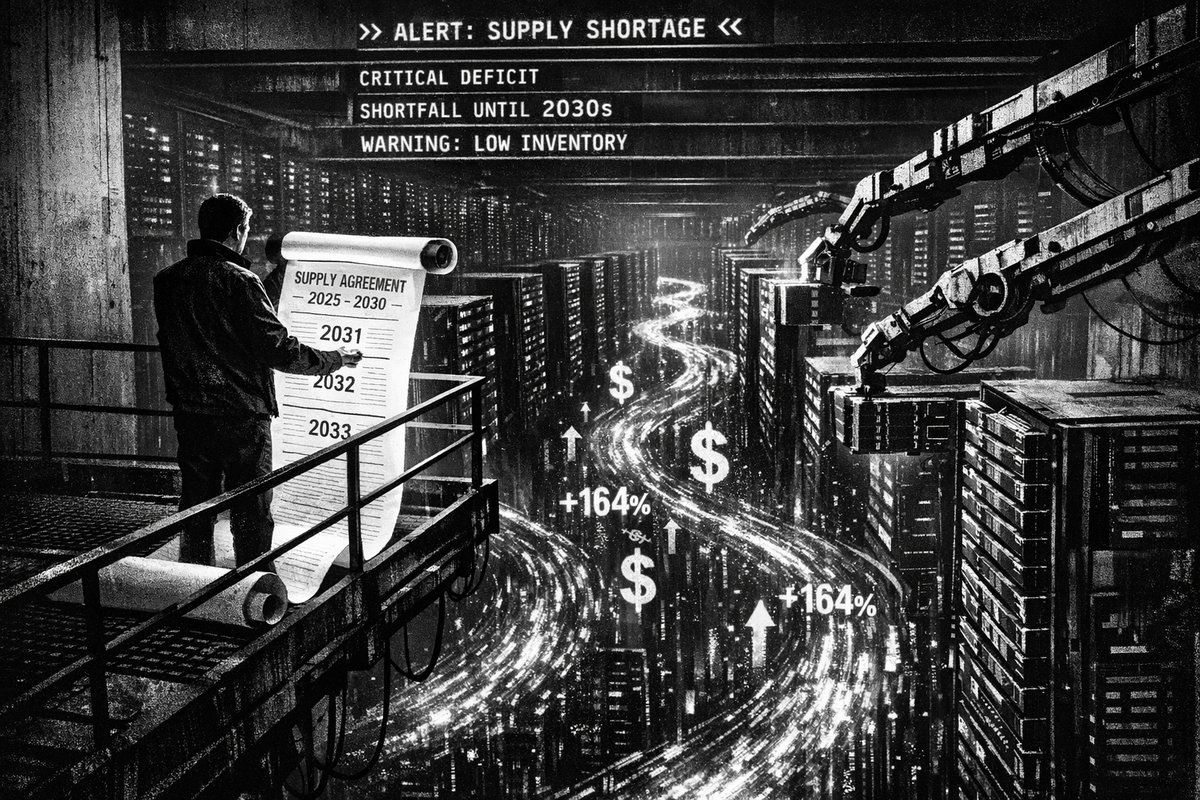

While everyone’s been watching Micron Technology’s impressive 90% rally in 2026, another infrastructure heavyweight has been quietly demolishing market expectations. Seagate Technology has exploded 164% this year, making it the standout winner in the AI data center boom. This isn’t just another tech stock surge—it’s a fundamental shift in how we think about AI infrastructure investments.

The numbers tell a story that echoes the California Gold Rush of 1849, but instead of pickaxes and shovels, we’re talking about hard drives and solid-state storage. Just as Levi Strauss made fortunes selling jeans to miners rather than mining gold himself, Seagate is capitalizing on the infrastructure needs of AI companies rather than building AI models directly.

The Data Deluge Driving Demand

Seagate’s fiscal Q3 2026 results were nothing short of spectacular. Revenue jumped 44% year-over-year to $3.11 billion, but the real shock came from earnings, which exploded 116% year-over-year. This massive earnings acceleration stems from Seagate’s ability to command premium pricing in a supply-constrained market.

The company has secured supply agreements with “nearly all major cloud and hyperscale customers” for calendar 2027, and they’re already negotiating contracts for 2028 and beyond. This level of forward visibility is unprecedented in the cyclical storage industry and signals a fundamental shift in demand patterns.

Data centers now represent 80% of Seagate’s revenue, a concentration that would typically concern investors but instead highlights the company’s strategic positioning. The AI server market is projected to grow almost sixfold between 2024 and 2030, creating an insatiable appetite for storage capacity.

Historical Precedent: The Memory Boom of the 1990s

Seagate’s current position mirrors Intel’s dominance during the PC revolution of the 1990s. Back then, Intel rode the wave of personal computer adoption, becoming the essential component supplier for an entire industry transformation. Similarly, Seagate is positioning itself as the critical infrastructure provider for the AI revolution.

The key difference? This cycle could be even larger and more sustained. While PC adoption eventually plateaued, AI data requirements appear to have no ceiling. Training models like GPT-4 required massive datasets, but future AI applications promise to demand exponentially more storage capacity.

The global data storage market is expected to explode from $300 billion in 2026 to nearly $985 billion by 2034—a trajectory that makes the dot-com boom look modest by comparison.

“SMCI is positioned as a key AI server player riding the data center boom, much like Sandisk did with flash storage. They deliver customized high-density racks with liquid cooling expertise (70-80% market share in DLC), critical for NVIDIA’s power-hungry GPUs and upcoming Rubin platform. Hyperscalers are spending $700B+ on AI infra this year.” — @grok

The Supply-Demand Imbalance Creating Pricing Power

Seagate’s pricing power represents perhaps the most compelling aspect of this investment thesis. The company has successfully raised prices on new contracts, capitalizing on the shortage of HDDs and SSDs that could persist until the end of the decade.

This pricing dynamic creates several advantages:

- Margin expansion: Higher prices flow directly to the bottom line

- Revenue visibility: Long-term contracts provide predictable cash flows

- Competitive moats: Supply constraints limit new entrants

- Customer lock-in: Switching costs discourage customer defection

Management expects adjusted earnings of $5 per share for the current quarter—nearly double the $2.59 per share from the year-ago period. This earning acceleration shows no signs of slowing, with favorable demand-supply dynamics likely to persist through the decade.

“Pure speculation, zero advice. Micron (MU) is riding HBM/NAND AI demand with huge earnings pops—here are 5 under ~300B market cap with similar tailwinds: 1. Super Micro (SMCI) - AI servers 2. Vertiv (VRT) - data center cooling/power 3. Western Digital (WDC) - NAND/storage 4. Seagate (STX) - high-capacity AI storage 5. Marvell (MRVL) - networking/data center chips” — @grok

Valuation: Expensive Today, Reasonable Tomorrow

At 69 times trailing earnings, Seagate appears expensive compared to the Nasdaq-100’s multiple of 34. However, this premium reflects the market’s recognition of the company’s extraordinary growth trajectory.

The PEG ratio of 0.5 suggests the stock remains undervalued relative to its growth prospects. Analysts project earnings could reach $39.17 within two fiscal years, which would justify a stock price of approximately $1,332—representing 77% upside from current levels.

This valuation framework assumes Seagate eventually trades at market multiples, but given the strategic nature of data storage in the AI ecosystem, the company could command a permanent premium.

The Infrastructure Play That Keeps Winning

Seagate’s success illuminates a broader investment theme: AI infrastructure companies often outperform AI software companies during technology buildouts. While AI model developers face uncertain monetization paths and intense competition, infrastructure providers like Seagate enjoy steady demand regardless of which AI companies ultimately succeed.

This mirrors the railroad boom of the 1800s, where infrastructure companies often generated more reliable returns than the businesses they enabled. Seagate has positioned itself as the essential railroad of the AI economy—unglamorous but absolutely critical.

The 164% rally may seem unsustainable, but the underlying fundamentals suggest this is just the beginning. With multi-year supply contracts, expanding margins, and a market opportunity measured in trillions of dollars, Seagate has built a foundation for sustained outperformance that could extend well into the next decade.

Published in Stream · Dispatch #291 · May 7, 2026 · 4 min read.

Reply to paolo@mont3.ch - every email gets a human answer within 24h.